Regularization and Cross-Validations#

When Linear Regression Fails #

In this context fails means that OLS is unable to provide a unique solution, such as a unique set of coefficients for the input variables.

Plain vanilla multiple linear regression (OLS) fails if the number of observations is smaller than the number of features.

Example: If the dependent variable is the Sales Price, we cannot uniquely determine the weights for the features if we have only 4 observations.

Dist. to School |

Prop. Area |

Housing Area |

Value |

Prop. Tax |

Bathrooms |

Sales Price |

|---|---|---|---|---|---|---|

7 |

0.4 |

1800 |

234 |

9.8 |

2 |

267.5 |

2.3 |

0.8 |

1980 |

244 |

10.5 |

2.5 |

278.2 |

4.3 |

1.1 |

2120 |

252 |

16.2 |

3 |

284.5 |

3.8 |

0.6 |

2500 |

280 |

18.4 |

3.5 |

310.4 |

Suppose we want to predict the “Sales Price” by using a linear combination of the feature variables, such as “Distance to School”, “Property Area”, etc.

The Ordinary Least Squares (OLS) method aims at finding the coefficients \(\beta\) such that the the sum or squared errors is minimal, i.e.

Important Question: Why does OLS fail in this case? Hint: the problem to solve is ill-posed, in the sense that it allows many perfect solutions.

What does Rank Deficiency mean, and why we need Regularization?#

The assumption for multiple linear regression is

where \(\sigma\) is the standard deviatin of the noise. Further, we assume that the “noise” \(\epsilon\) is independent and identically distributed with a zero mean.

We believe that the output is a linear combination of the input features.

Thus, if we would like to solve for the “weights” \(\beta\) we may consider

And if the matrix \(X^tX\) is invertible then we can solve for expected value of \(\beta\):

We can show by using Linear Algebra that the OLS solution obtained form minimizing the sum of the square residuals is equivalent.

We can test whether the matrix \(X^tX\) is invertible by simply computing its determinant and checking that it is not zero.

IMPORTANT: When the matrix \(X^tX\) is not invertible we cannot apply this method to get \(\mathbb{E}(\beta)\). In this case if we minimize the sum of the squared residuals the algorithm cannot find just one best solution.#

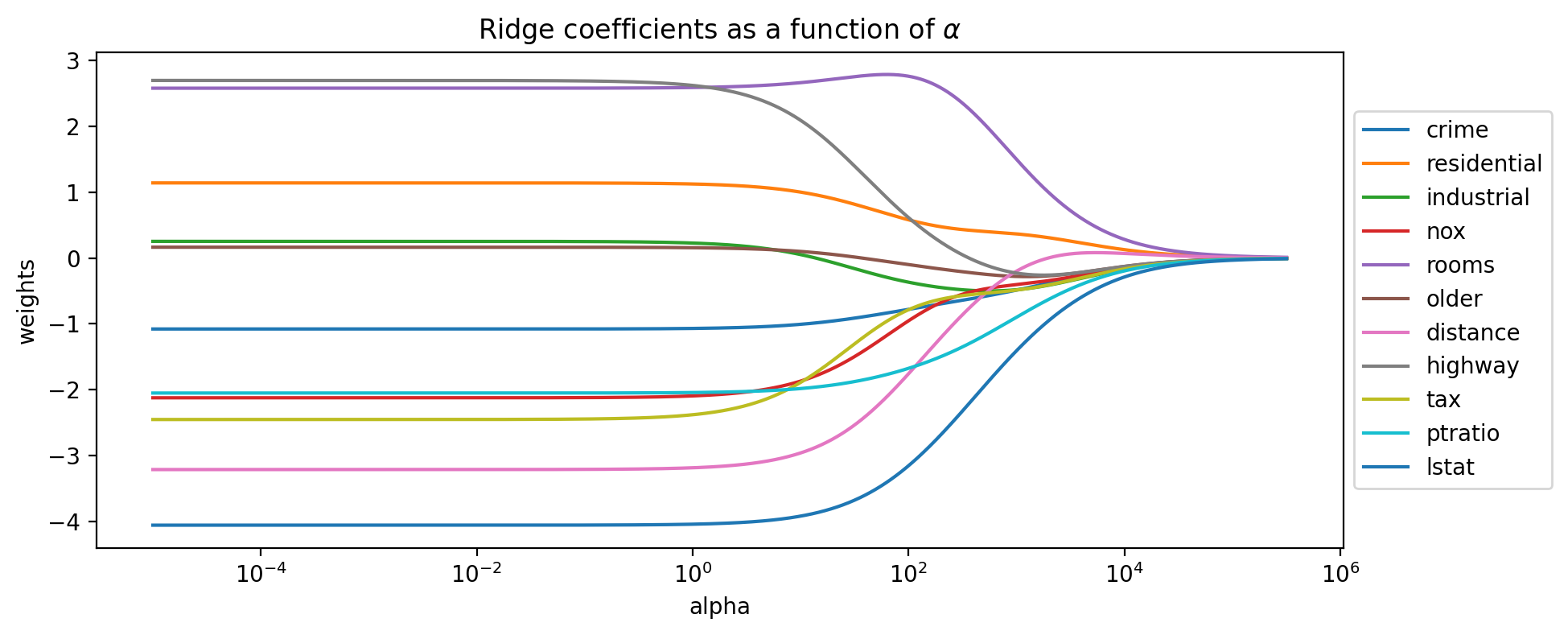

A solution for rank defficient Multiple Linear Regression: L2 (Ridge) Regularization#

Main Idea: minimize the sum of the square residuals plus a constraint on the vector of weights#

The L2 norm is

The Ridge model (also known as the Tikhonov regularization) consists of learning the weights by the following optimization:

where \(\alpha\) is a constant that can be adjusted based on a feedback loop so it is a hyperparameter (“tunning” parameter).

This optimization is equivalent to minimizing the sum of the square residuals with a constraint on the sum of the squared weights

subject to

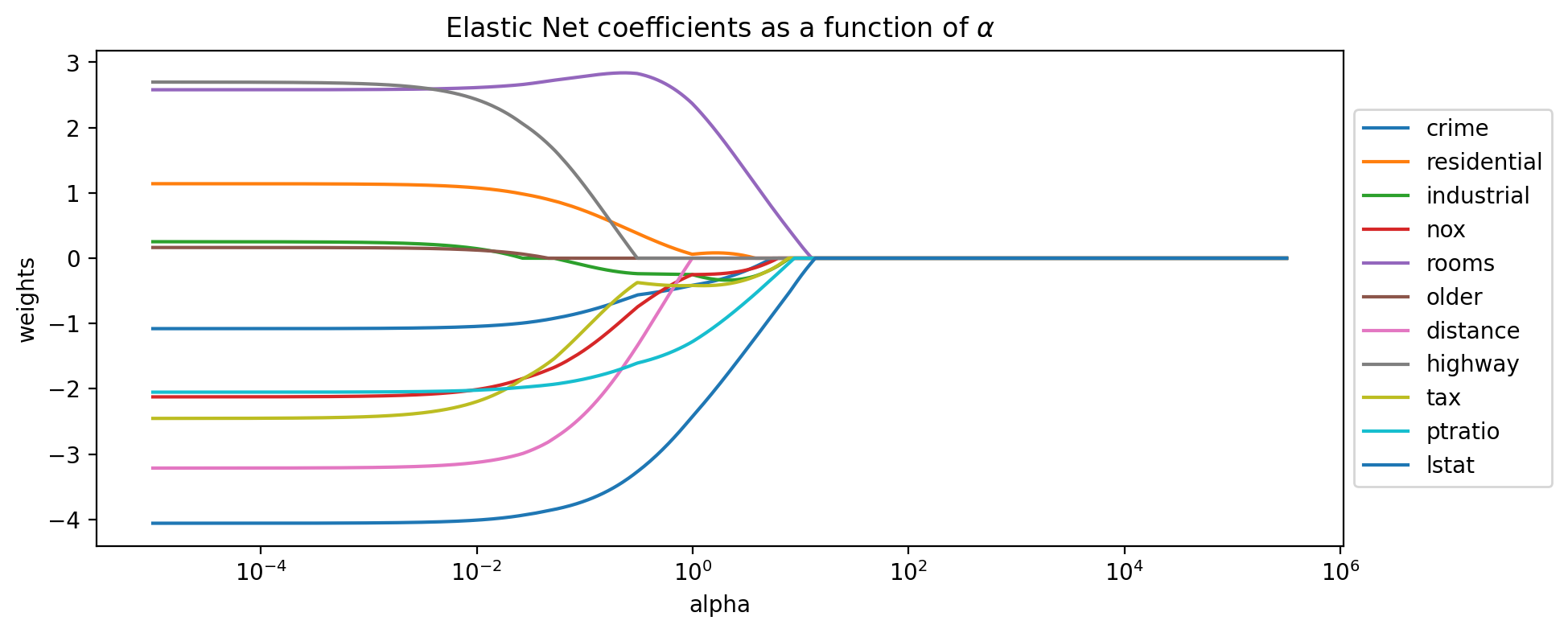

Important: What happens with the solution \(\beta\) when the hyperparameter \(\alpha\) grows arbitrarily large? Hint: generate a mapping and plot the coefficient paths.

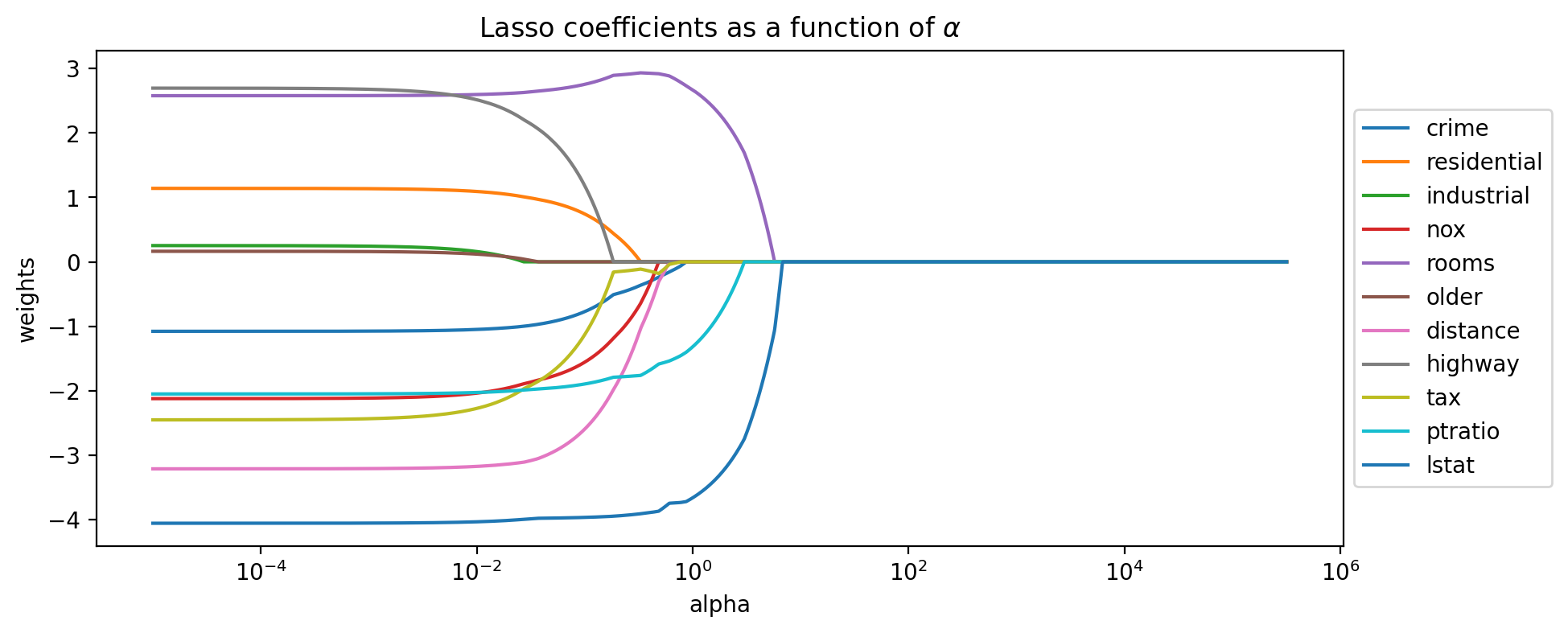

L1 (Lasso) Regularization#

The L1 norm is

The Lasso model consists of learning the weights by the following optimization:

where \(alpha\) is a constant that can be adjusted based on a feedback loop so it is a hyperparameter.

This optimization is equivalent to minimizing the sum of the square residuals with a constraint on the sum of the squared weights

subject to

The difference between L1 and L2 norms #

In the following example the L2 norm of the vector \(\vec{AB}\) is 5 and the L1 norm is \(4+3=7\).

Geometric comparison in 2D between L1 and L2 norms#

Elastic Net Regularization #

Tha main idea is to combine the L2 and L1 regularizations in a weighted way, such as:

Here \(0\leq\lambda\leq1\) is called the L1_ratio.

The Elstic Net regularization consists of learning the weights by solving the following optimization problem:

So with this rgularization approach we have two hyperparameters that we need to decide on.

Model Validation via k-Fold Cross-Validations#

In general: how do we know that the predictions made are good?

For many applications you can think of a data set representing both “present” and “future.”

In order to compare the predictive power of different models we use K-fold cross-validation.

How do we get unbiased estimates of errors?

Example schematic of 5-fold cross-validation:

Coding Applications #

Setup#

import os

if 'google.colab' in str(get_ipython()):

print('Running on CoLab')

from google.colab import drive

drive.mount('/content/drive')

os.chdir('/content/drive/My Drive/Data Sets')

!pip install -q pygam

else:

print('Running locally')

os.chdir('../Data')

%matplotlib inline

%config InlineBackend.figure_format = 'retina'

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

import statsmodels.api as sm

from sklearn.model_selection import RepeatedKFold

from sklearn.model_selection import KFold

from sklearn.model_selection import train_test_split as tts

from sklearn.metrics import mean_squared_error as mse

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import cross_val_score

from sklearn.linear_model import ElasticNet, Ridge, Lasso

Data Import#

data_housing = pd.read_csv('../Data/housing.csv')

data_concrete = pd.read_csv('../Data/concrete.csv')

Coefficient Paths#

feats = ['crime','residential','industrial','nox','rooms','older','distance','highway','tax','ptratio','lstat']

X = data_housing[feats]

y = data_housing['cmedv'].values

scale = StandardScaler()

Xs = scale.fit_transform(X)

# generate the coefficients for Ridge regression and many values of alpha

n_alphas = 2000

alphas = np.logspace(-5, 5.5, n_alphas)

coefs = []

for a in alphas:

ridge = Ridge(alpha=a, fit_intercept=False)

ridge.fit(Xs, y)

coefs.append(ridge.coef_)

# Display coefficient paths Ridge

plt.figure(figsize=(10, 4))

ax = plt.gca()

ax.plot(alphas, coefs)

ax.set_xscale('log')

plt.xlabel('alpha')

plt.ylabel('weights')

plt.title('Ridge coefficients as a function of $\\alpha$')

plt.axis('tight')

plt.legend(feats, bbox_to_anchor=[1,0.5], loc='center left')

plt.show()

# generate the coefficients for Ridge regression and many values of alpha

n_alphas = 2000

alphas = np.logspace(-5, 5.5, n_alphas)

coefs = []

for a in alphas:

model = Lasso(alpha=a, fit_intercept=False)

model.fit(Xs, y)

coefs.append(model.coef_)

# Display coefficient paths Ridge

plt.figure(figsize=(10, 4))

ax = plt.gca()

ax.plot(alphas, coefs)

ax.set_xscale('log')

plt.xlabel('alpha')

plt.ylabel('weights')

plt.title('Lasso coefficients as a function of $\\alpha$')

plt.axis('tight')

plt.legend(feats, bbox_to_anchor=[1,0.5], loc='center left')

plt.show()

# generate the coefficients for Ridge regression and many values of alpha

n_alphas = 2000

alphas = np.logspace(-5, 5.5, n_alphas)

coefs = []

for a in alphas:

model = ElasticNet(alpha=a, fit_intercept=False)

model.fit(Xs, y)

coefs.append(model.coef_)# generate the coefficients for Ridge regression and many values of alpha

n_alphas = 2000

alphas = np.logspace(-5, 6, n_alphas)

coefs = []

for a in alphas:

ridge = Ridge(alpha=a, fit_intercept=False)

ridge.fit(Xs, y)

coefs.append(ridge.coef_)

# Display coefficient paths Ridge

plt.figure(figsize=(10, 4))

ax = plt.gca()

ax.plot(alphas, coefs)

ax.set_xscale('log')

plt.xlabel('alpha')

plt.ylabel('weights')

plt.title('Elastic Net coefficients as a function of $\\alpha$')

plt.axis('tight')

plt.legend(feats, bbox_to_anchor=[1,0.5], loc='center left')

plt.show()